New DMS Report: Best DMS Vendors to Chase $541M US Growth till 2027

If you have been visiting the annual NADA Conventions, you get a sense that the universe of dealership software is growing by the minute. Additional exhibitor floor space, more educational sessions (many provided by vendors), bigger vendor booths, and more tech buzz. Our 2022 DMS Report breaks down the DMS segment, best DMS vendors, DMS market forces, and DMS future trends. Our taxonomy of DealerTech (primarily for Franchised Car) now includes more than 40 categories with over 800 vendors. You can learn more here.

DMS = DealerTech Heart & Central Nerve System:

The Dealer Management System (DMS) is the heart of everything that embodies dealership software. The DMS is a mandatory application that every Franchised dealer needs to connect with their respective OEMs. It is also an ERP suite touching more than 75% of the dealership employee base – from Dealer Principal to technicians. Accordingly, the DMS was able to drive up pricing to become a dealership’s most expensive software tool.

Besides powering almost every muscle in the dealership (as a heart would do), one could also describe the DMS as the central nervous system. The DMS hosts crucial operational data points related to sales and service transactions, and to master data like vehicles and customers.

Hence, a discussion about dealership data (e.g., as it relates to data integrity, data safeguards, data governance) and layered applications (as it relates to 3rd Parties and its data integration) as a whole is inadvertently a discussion about the DMS.

The DMS Oligopoly is Dead:

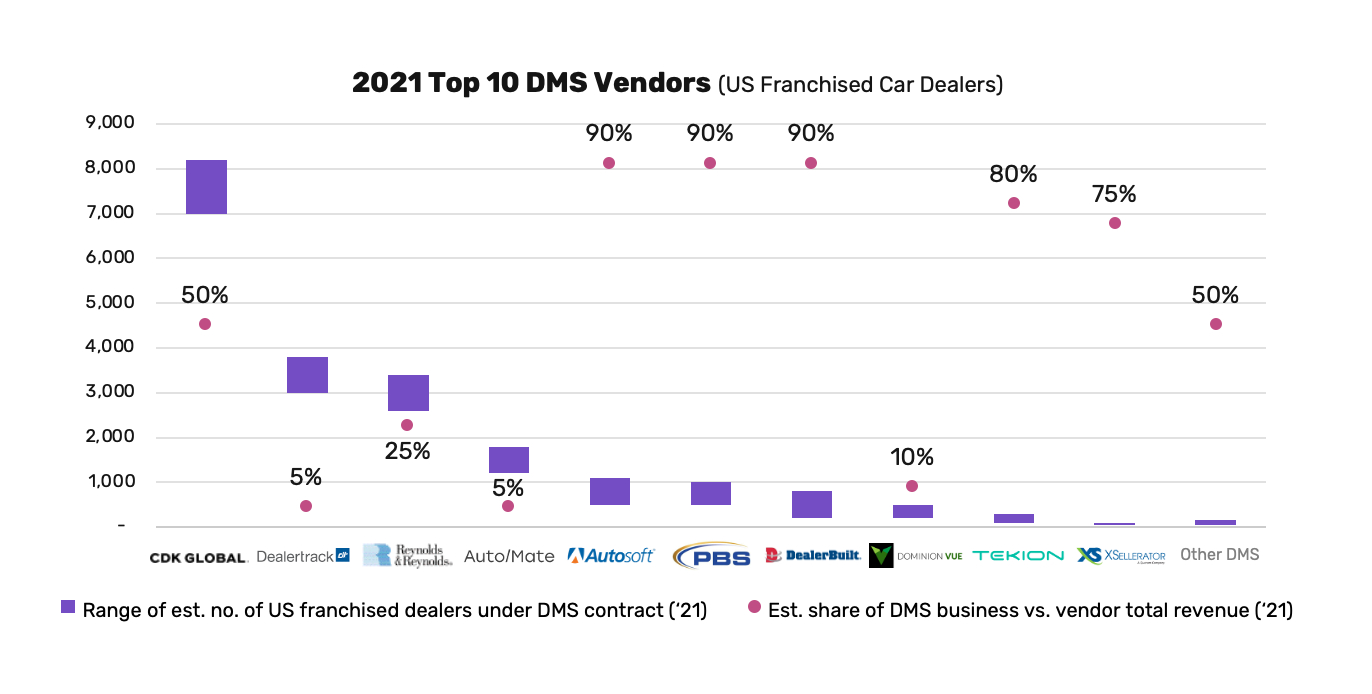

The times of two dominating DMS vendors are long gone (for Franchised Car in the US). As our 2022 DMS Report lays out, if you are a dealer looking for DMS alternatives, there has never been a better time to shop for your DMS. As a Franchised Car dealer, you can choose between ten or more solutions, each with a robust set of features to make it work. Of course, the final DMS relevant set depends on your decision-making points and workflow requirements. But you have choices that bring favorable terms in a proper call for tenders. Pricing for core DMS features is compressed and aggressive. Contractual obligations are getting better too. Seize the moment!

Graph 1: 2021 Top 10 DMS Vendors (US Franchised Car Dealers)

DMS and DealerTech Leaders:

CDK – New Beginning Under Brookfield:

For CDK to become a private company (again) has been in the making for a while. And it makes sense for them: less public scrutiny, less growth story, less shareholder value. Certainly, Brookfield wants its money’s worth. Margins are semi-optimized after dumping International DMS and Digital Marketing. The team around reappointed CEO Brian MacDonald has a plan to execute. The question is, what move to make next. CDK is a true Auto Retail Enabler with many software applications. Yet, how can CDK compete in a new mobility economy? A data and API play around Fortellis, Neuron, and Square Root is likely not enough.

Dealertrack DMS – Avoid the Plateau:

What’s there to say? Dealertrack DMS is number two. Cox Automotive’s cross-selling with a narrative around volume discount, single sign-on, no integration fees, and singular customer view works. If a dealer already has VinSolutions, vAuto, Xtime, Dealer.com, Autotrader,… then Dealertrack DMS seems a natural extension. That’s why CDK, R&R, Solera, and Co. borrow the ecosystem spiel. While Cox drives full steam ahead on its New Mobility division and mission, the company’s innovation mainly happens outside the DMS. That’s a shame: DMS market leader ambitions on a tight budget is a utopian formula for success. What’s the long-term DMS vision for Dealertrack?

R&R – Unchained (Life After Bob):

It’s hard to watch Bob Brockman’s free fall. But I can’t deny feeling happy for the people and dealers of The Reynolds and Reynolds company. There is hope and enthusiasm that I haven’t seen before. Tommy Barras and Chris Walsh embrace the change and life without dealer talk tracks and objections overcoming. The new mantra seems to be: do what’s right or needed – considering the bleeding of dealers over the last decade. There is a new approach to R&R contract extensions with sincere conversations about dealer pain points, simplified terms and conditions, and more flexibility on price and contract length. There is even talk about DMS competitor unhooks!

Auto/Mate – Small Fish in a Big Solera Pond:

After its acquisition by DealerSocket, Auto/Mate is now fully folded into the Solera galaxy. The once so personal and happy dealer family sentiment feels now more corporate. There is nothing wrong with grand plans. The chase for layered apps and ecosystem narrative continues and is now complemented by the other Solera BUs like autopoint. Like Cox, Solera is all-in on new mobility as the company made vital acquisitions with fleet and mobility players Spireon and Omnitracs. They now even have a lending division. As a dealer, you can earn a free DMS ticket if you sell enough cars with Solera Auto Finance. This giant is just awakening.

If you want to learn more about our 2022 DMS Report, take this shortcut. Our market study is a true labor of love and genuinely comprehensive. Thank you for all the support and inspiration!

DMS Challengers:

Tekion – Roaring, and Soaring:

Tekion is here to stay and surfing comfortably on the DMS disruptor wave. There is some true innovation and a fresh impulse shaking up the DMS segment. Growth is supposedly coming from everywhere – legacy DMS and other challengers. One cannot deny sympathizing with the story and ROI for early investors. But how the valuation lines up with the reality of the DMS market is a very different story. There is IMMENSE pressure to make the economics work – probably beyond 5,000 dealers and $15k MRR per dealer site. We are off by years.

AutoSoft – Ready to GO:

Similar to Tekion, PBS, and DealerBuilt, the new AutoSoft GO vision is to embrace a superior User Experience. Cloud-native, simplified one-screen navigation, highest security standards, smart layered apps to replace legacy bolt-ons. The only problem is – to speed up the OEM certifications. I hear different voices, with some blaming OEMs for preferential DMS treatment (i.e. Tekion).

PBS – Canadian DMS Leadership and Hospitality:

Quietly but with dedication, PBS has added a solid DMS footing in the US. Some came from acquisitions, and plenty came from conquest Sales. PBS was an early embracer of the One platform approach. That’s how many Canadians like it, and plenty of US dealers. The v10 system has deep business rules, layered apps, and fair pricing and terms. This company is growing.

DealerBuilt – Customer Experience and Engagement DMS:

CEO Mike Trasatti talked about the ceDMS and engagement features before others embraced the narrative. DealerBuilt is probably also one of the best DMS to accommodate flexible business rules across departments and one of the best DMS to co-innovate with. DealerBuilt has always looked out for both dealers and partners. That’s the only way forward, and others should follow their example.

Dominion – Fresh VUE with Ambitions:

Dominion is not short of patience and persistence. They want to get DMS VUE right. And it looks like they are on track. Some decisions hurt (no Vision CRM anymore), and others came easy (e.g., fully embedded UpdatePromise Service tool). Considering the other pieces from Dominion Dealer Solutions, VUE has a launchpad to steal some market share. Probably on the lower end of the market, but that tail is long.

Quorum – Canadian Family of Brands:

Maury Marks has a good sense of opportunities. He surrounded himself with smart people and made big-impact additions. DealerMine did not just add a Service CRM but also a virtual BDC. AutoVance added DR, Desking, and F&I capabilities, which somehow seem tough to crack in Canada. Now, they added an accessory play that lends itself nicely to dealerships’ brick-and-click businesses. Quorum appears to have good pieces together to be sticky.

Yes, there are more DMS vendors in the US and CA. And without a doubt, they have distinctive value propositions. DMS Consultant Sandi Jerome is now retired after handing DealerStar over to DealerTeam (Salesforce base). Advent Resources – mostly known for F&I – also tried to take a run at DMS (and CRM). Serti from keyloop is big in French-speaking Quebec. And don’t forget about Adam Systems, MPK,…

Positive DMS Outlook:

There is lots of DMS growth until 2027. Per our 2022 DMS Report, we are estimating the growth at 6.7% CAGR or $541M. It’s not coming from an increase in the dealership base, which has been stable at 0% CAGR over the last ten years (per NADA). It’s also not coming from DMS price increases and escalators (although inflation is substantial). No surprise, but the lift will come from higher penetration of layered apps.

That builds pressure on DMS vendors to offer competitive layered apps and bolt-on providers to create defendable value propositions. Perfect breeding ground for progress. Eventually, it becomes a quest for differentiation for leading DMS providers and DMS challengers alike.

I can’t wait to see everyone in Dallas next year for the 2023 NADA Convention. I am sure we will see DealerTech rollups till then and new ways to compete in the DMS space. The pie is big enough.