Why Digital Retail is a Dead-End

When I reviewed Digital Retail (DR) providers just last year, I quickly learned this segment contains players from different corners of the DealerTech universe. Digital Retail solution providers originated from e-commerce, FinTech, website and online management, conversational solutions (like chat), and even management systems (think DMS, CRM). For a few trailblazers, DR was their sole product. For others, it was a layered app and add-on solution to their existing offering. Not surprising that many of the latter decided to make Digital Retail their new lighthouse merchandise, following last year’s industry-wide cry for zero contact sales. COVID-19 created the business case for them. Depending on your definition, today’s count of Digital Retail providers lands between 25 to 30 companies. I have talked to industry peers that estimate the count to exceed 60. Despite the attention and growth, here is my take on why Digital Retail is a dead-end.

Recent Digital Retail Investments and Roll-Ups:

Naturally, with many players entering, the DR space got crowded quickly. Some of us could argue, this segment has many new entries because it will produce many exits. Here is some context:

- Modal: $15M Series A led by American Honda in 12/20

- Prodigy Software: acquired by Upstart for an undisclosed amount in 3/21

- CarNow: $30M investment from Battery Ventures in 5/21

- Roadster: acquired by CDK Global for $326M in 6/21

- Gubagoo: acquired by R&R for an undisclosed amount in 6/21

- Motoinsight: acquired by TRADER Corporation for an undisclosed amount in 6/21

- Darwin Automotive (SIS): acquired by J.D. Power for an undisclosed amount in 7/21

- truPayments: acquired by PureCars for an undisclosed amount in 7/21

- Rodo: Series B led by Holman Strategic Ventures, Evolution VC Partners for $18M in 7/21

- FUSE Autotech (Walser Automotive Group): $10M Series A led by Target Global

- CreditIQ: acquired by CARS for $30M at closing

The oracle from Trenton, MI, Cliff Banks, reports that the acquisitions that transpired between June and July 2021 totaled approximately $1.2B. Read more here.

Not only did it get busy quickly in Digital Retail, but it also got fierce. Great news for dealers, not-so-good news for providers. Because with lots of competition comes price pressure. Although we are likely far away from saturation, the once skyrocketing rate of adoption for Digital Retail has probably flattened over the past three months. At this stage in the COVID-19 pandemic, if dealers have not jumped on the DR train yet, the chances are that the laggards may do slowly. So, I wonder how much of the remaining white space is obtainable for DR providers in the next 12-24 mo. Market share may primarily come from conquest. Are we already in the midst of a rip-and-replace phase where dealers jump ship?

1) Digital Retail is Omni-Retail:

Digital Retail is a dead-end because it has never been about “Digital” in the first place. Despite low e-commerce penetration in automotive retail as Carvana, SHIFT and VROOM like to lay out in their investor pitches, buying a car will remain a multi-touchpoint experience for the foreseeable future. Yes, 5% of consumers want to check out online and get delivery without test-driving, but most still want to conduct their second most expensive purchase in their life in person. Arguably, they want to do it faster and more conveniently from home. What “Digital Retail” could deliver is a revolving door that ties all sales touchpoints together regardless if prospects enter the dealership via self-service online, in-store, or anywhere in between.

2) Digital Retail on a One-Way Product Road(map):

Digital Retail – as a software category – is a dead-end because it has a limited path forward unless merged.

All DR providers are checking off the same boxes in their enhancement cycles: virtual garage, soft vs. hard credit score, credit app, desking engine for penny perfect numbers, in-store presentation tool or kiosk, online F&I Menu presentation, trade-in appraisal and cash offers, accessories, contracting and e-signing, checkout page with payment, delivery scheduling, retargeting features,… Will anyone have a defendable differentiation in 5 years?

This confinement makes me believe that Roadster and Gubagoo are a bargain for the acquired, not the buyers. As part of platforms – just like Cox Automotive does with Dealer.com and its other sister companies – you can fold Digital Retail into a larger customer and opportunity management approach. Exit barriers come from advanced integrations within the family apps and potentially new use cases (e.g., transplanting a Digital Retail perspective to a Digital Service experience). So what will become of the remaining players in Digital Retail once the last checkboxes are cleared? Digital engagement tools merging with AdTech, Omni-retail solutions melding with CRM, transactional platforms absorbing Desking, Lending as a Service platform combining with credit and compliance solutions?

3) Digital Retail Belongs to the OEMs:

Digital Retail for dealers is a dead-end because your friendly next-door neighbor OEM will take over your digital (EV) sales.

Many dealers tell me about the same challenge: how to decide on one DR vendor across multiple brands? Do they sacrifice a cohesive dealership brand experience over OEM money and preferential treatment? I wonder if Digital Retail is becoming the next website disaster. Does every dealer need two active Digital Retail tools? One that dealers pick by choice, and one to comply with OEM rules. Don’t forget to slap that Capital One Navigator as another DR customer (tr)app on your homepage. The third time’s a CX charm.

For national retailers, this decision is more straightforward. They have the funds and strategic position to aspire for their own branded Customer Experience regardless of OEM interest. Asbury rolled out Clicklane powered by Gubagoo (now R&R). Lithia released Driveway running on a proprietary engine and Shift Technologies. Penske just announced it would power carshop through Cox Automotive’s new Esntial Commerce.

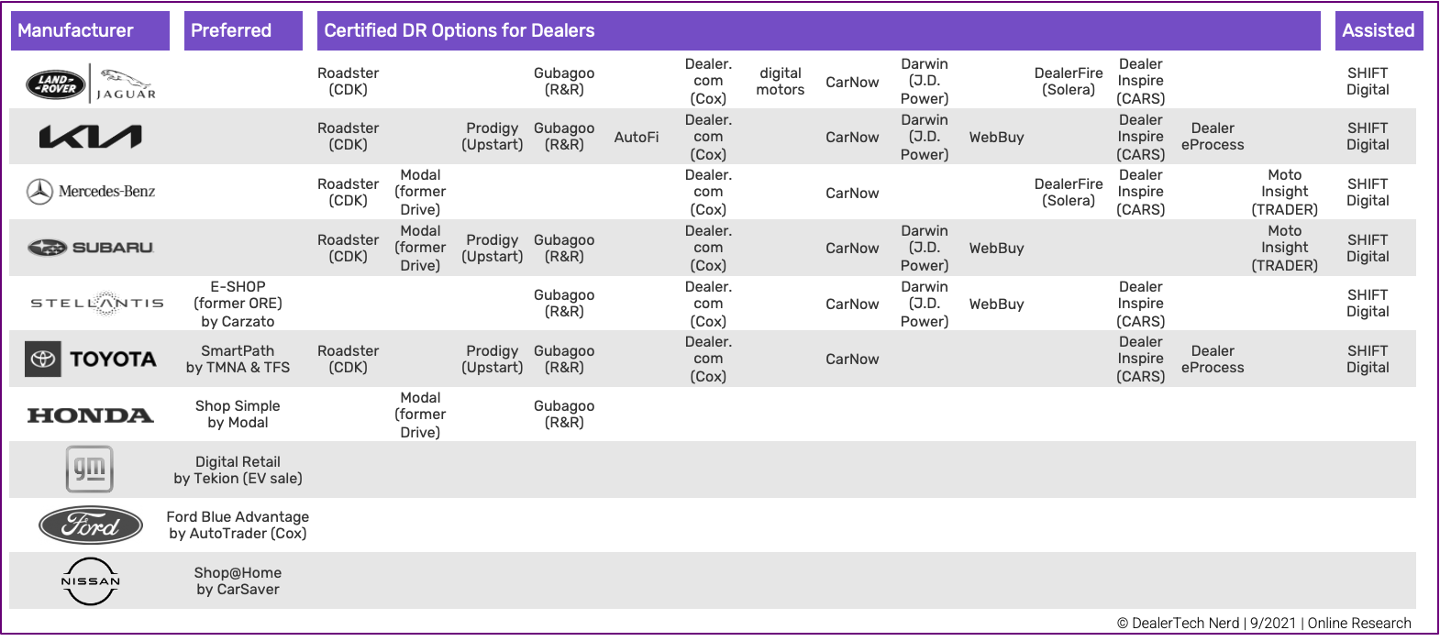

Manufacturers follow different strategies to digitize and unify the car buying experience across their dealer body. Some of them certify several DR tools and offer dealers plenty of choices. For example, Kia certified ten (10) DR vendors – no other brand has more. Other OEMs approve less while also pushing for one preferred option. Think of Stellantis that offers dealers six (6) certified DR tools besides its highly endorsed new E-SHOP (former ORE Online Retail Experience) by Carzato. And there are other OEMs with only one endorsed DR tool. That can either be a strategic partner (like Nissan with Shop@Home by CarSaver) or an asset (like Shop Simple by Modal from American Honda or General Motors tool powered by Tekion).

Table 1: OEM Preferred Digital Retail Options

Notably, OEMs seem to seek external assistance to select and manage Digital Retail providers whenever DR dealer choices are plentiful. Shift Digital is a popular partner for many of those OEMs. The company from Birmingham, MI, recently came under scrutiny when VW reported a data breach at a vendor that impacted 3.3 million people in North America. Per an internal email and reported by Automotive News, this vendor was identified as Shift Digital.

4) Digital Retail Powered By Marketplaces and Lenders:

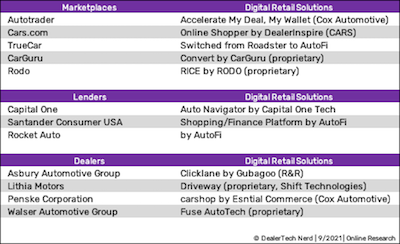

Besides manufacturers courtshipping online car shoppers, both marketplaces and lenders aim so too. Some seek partnerships with Digital Retail vendors. TrueCar was running on Roadster and just announced a switch to AutoFi’s Lending as a Service. Santander Consumer USA also partnered with AutoFi. So did Rocket Auto.

Others are building out their own DR engines. Autotrader, CarGurus, Rodo, and Capital One all created in-house software. Cars.com runs on its DealerInspire DR engine and may add features from the newly acquired CreditIQ solution (e.g. the Lending-as-a-Service framework). Despite good DR white-label options, CEOs may reckon that higher valuations come from proprietary DR applications. Supposedly, it makes for a better investor story.

Table 2: Digital Retail Solution of Marketplaces, Lenders and Dealer Groups

This arena will remain hot for investment and roll-ups. I am sure more money will go down this DRain.